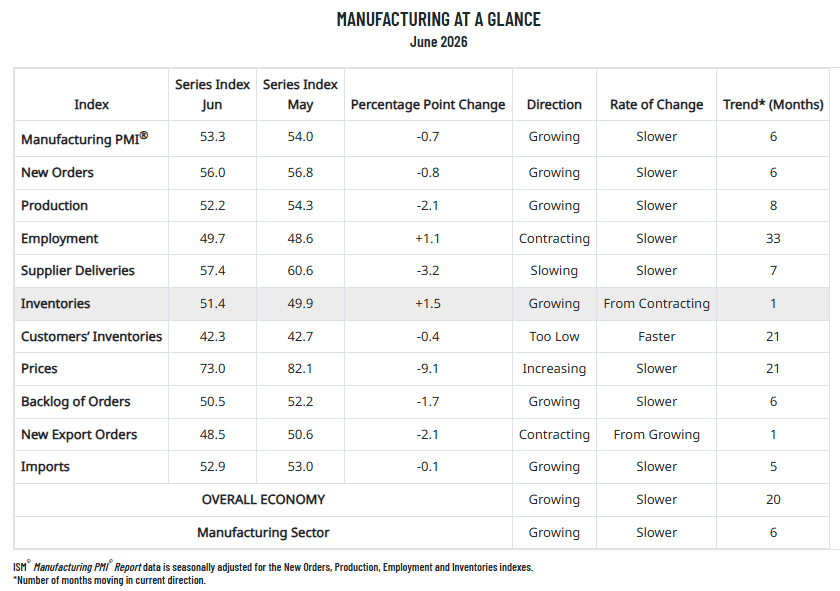

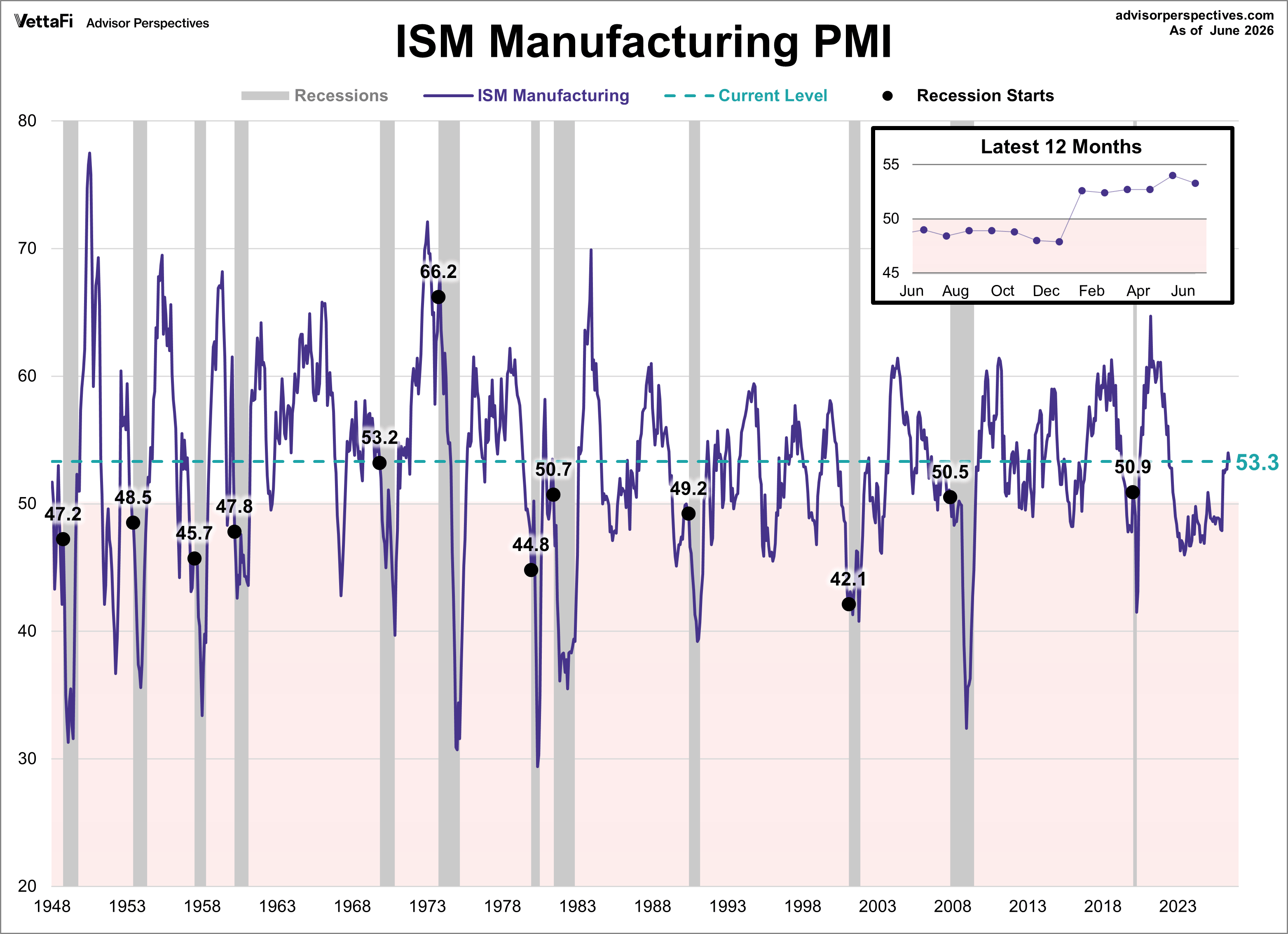

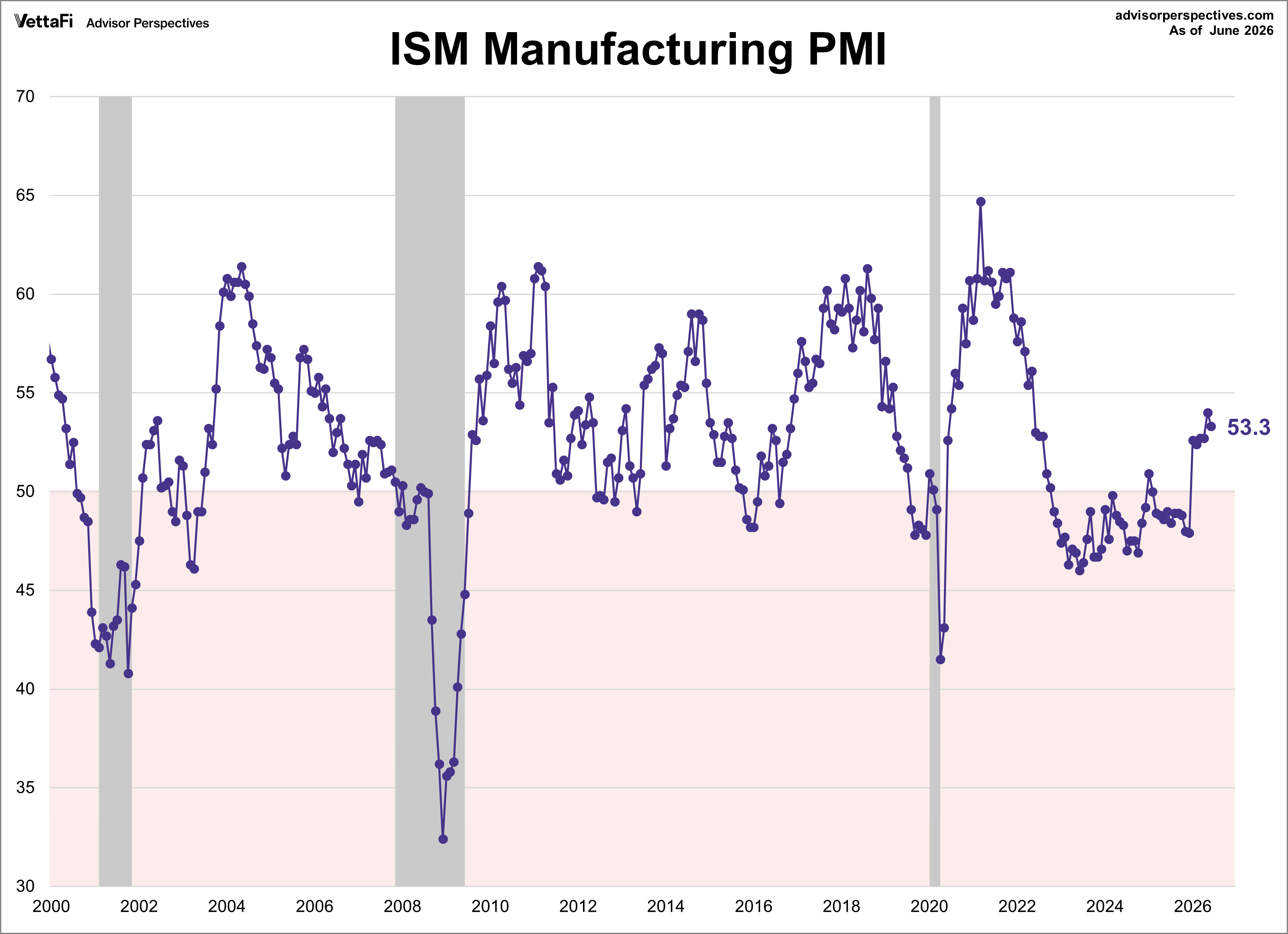

The Institute for Supply Management (ISM) manufacturing purchasing managers index (PMI) came in at 53.3 in June, down from 54.0 in May, marking slightly slower growth. The latest reading was just below the 53.8 forecast and is the index's sixth straight month in expansion territory.

Here is an excerpt from the latest report:

Spence continues, “In June, U.S. manufacturing activity remained in expansion territory, growing at a slightly slower pace as compared to the month before. Of the five subindexes that make up the PMI®, the New Orders and Production indexes grew slower as compared to the previous month, the Supplier Deliveries Index slowed at a slower rate, and the Employment and Inventories indexes improved with the latter entering expansion territory.

“In June, 34 percent of the comments were positive and 66 percent negative, with a 1-to-1.9 ratio of positive to negative sentiment. Among negative comments, the Iran war was mentioned in 31 percent and tariffs in 17 percent; 50 percent of the panelists mentioned pricing volatility as an issue for their companies.

“In June, two of four demand indicators (New Orders and Backlog of Orders) were in expansion, and the Customers’ Inventories Index remained in ‘too low’ territory, contracting at a faster rate. A ‘too low’ status for the Customers’ Inventories Index is usually considered positive for future production. New Export Orders returned to contraction, losing 2.1 percentage points since May.

“Regarding output, the Production Index is in expansion for the eighth month in a row, and the Employment Index increased by 1.1 percentage points but remained in contraction. Among panelists, 36 percent indicated that managing head counts remains the norm at their companies, while 64 percent are hiring — a near reversal of those numbers from the start of the year (66 percent of companies were managing staff levels in the January report).

“Finally, inputs (defined as supplier deliveries, inventories, prices, and imports) were mixed, with the Supplier Deliveries Index decreasing 3.2 percentage points, the Inventories Index entering into expansion, the Imports Index losing 0.1 percentage point but staying in expansion, and Prices Index relief coming with a 9.1-percentage point drop, a reading of 73 percent versus 82.1 percent in May."