- EM should continue to benefit from a number of positive fundamental and technical forces that are not expected to abate anytime soon.

- We continue to see a meaningful bifurcation between the investment-grade-rated and high-yield-rated segments, which is the natural evolution of any growing bond market.

- For now, it makes sense to focus on USD-denominated EM sovereign and corporate debt for their more defensive qualities — and playing EM local markets tactically.

Robert O. Abad

23 Years Experience

Western Asset Management

Company

Portfolio Manager, 2006–

Citigroup Investment Banking

Senior Credit Officer and Market

Risk Manager, 2002–2006

Fiduciary Trust International

Investment Strategist, 1999–2000

Global Emerging Markets

Advisors, L.P.

Assistant Portfolio Manager,

1995–1999

Merrill Lynch & Co.

Emerging Market Debt Analyst,

1991–1995

Equitable Insurance Companies

Analyst, 1989–1991

The Peter F. Drucker & Masatoshi Ito

Graduate School of Management

Adjunct Professor

Columbia University,

M.B.A., Masters in International

Affairs

New York University,

Bachelor of Science

In this Q&A, Western Asset Portfolio Manager Robert Abad discusses the latest dynamics and trends within emerging markets (EM). Although EM continue to demonstrate resiliency, Mr. Abad believes that given the amount of global uncertainty today, it is important that investors evaluate opportunities alongside a manager equipped to guide them through the risks and rewards of this evolving asset class.

Q: Given the uncertain global environment, is there the risk of a flight-to-quality away from EM debt?

A: We don’t foresee anything on the immediate horizon that would result in a full-scale retreat. During past EM crises, we would typically see a flight-to-quality of funds away from both EM debt and equity at the first sign of trouble, as investors sought the liquidity and relative safety of other traditional, “risk-free” asset classes. What we’ve been observing during recent periods of market duress is a flight-to-quality within EM—an intra-EM dynamic—where funds move out of higher beta sectors such as EM equity and EM currencies and move instead into lower beta sectors such as high-grade USD denominated EM sovereign and corporate credit. This isn’t surprising to us.

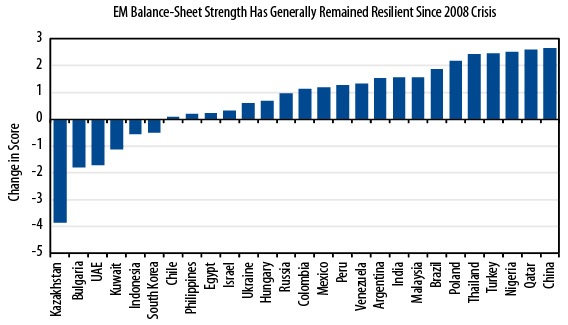

Prior to the S&P downgrade of the US last year, we argued that EM, as an asset class, had “graduated” on the global capital structure of risk—that the investment-grade tier of EM offered investors another viable fixed-income alternative with the defensive qualities of similarly rated, fundamentally sound developed market (DM) assets. This intra EM dynamic supports our argument, as well as our long-held thesis that EM experienced a “structural break” following the 2008 crisis; investors recognize that the stronger fundamental position of EM no longer justifies a wholesale liquidation of EM exposure during crises, nor an outsized spread premium relative to DM. If anything, this “upside-down” story—one of worsening DM fiscal balances and public debt-to-GDP1 levels versus EM—combined with strong, longer-term oriented flows into the EM asset class, should help forestall the kind of capital flight and severe spread volatility we observed in EM more than a decade ago.

Q: Is the rally in EM debt sustainable given its strong performance year-to-date?

A: EM should continue to benefit from a number of positive fundamental and technical forces that are not expected to abate anytime soon. At the top of this list is the resilience of EM growth, which has continued to surprise many observers, given that global growth forecasts continue to be revised lower. But as we’ve argued before, balance-sheet strength and policy flexibility matter more for EM in this global macro environment than does their ability to sustain the high growth rates to which investors have been accustomed. It’s the reason why EM have been able to weather the body blows coming from the US and Europe, and why EM debt has continued to outperform EM equities.

From a technical perspective, outperformance among EM since 2008 has attracted a diverse mix of new investment flows into the asset class. We continue to see a broadening and deepening of the EM investor base, with greater participation by longer-term oriented investors, such as US, European and Asian pension plans, insurance companies, sovereign wealth funds, and more activity from a more volatile base of Asian private bank clients, all of whom continue to search for yield and diversification in a world of decreasing supply of USD spread product.2 The presence and participation of these new investors, coupled with the reinvestment activity of existing investors who are benchmarked to EM debt indices, should continue to provide strong technical support for USD-denominated EM sovereign and corporate debt.

Q: Is the recent euphoria over EM justified?

A: It’s certainly justified given the strong fundamental improvements we continue to observe, among them, recent sovereign ratings upgrades in Turkey, the Philippines, Indonesia, and South Korea against a backdrop of more downgrades in the developed world. However, no one should be deluded into thinking that EM “decoupling” is real, that EM face no internal risks, or that EM are immune to external shocks such as a European banking crisis.

Strong global liquidity conditions, which can promote excessive domestic credit growth and artificially boost commodity prices, have played a critical role in the positive trajectory of EM over the past decade. However, financial history has shown that such conditions, when artificially sustained for an extended period of time, can produce negative outcomes. The eventual contraction of liquidity and its impact on domestic markets can fuel capital flight and balance of payments instability, especially in countries with weak political regimes, managed exchange rate regimes, volatile sources of export revenue, and/or fragile financial systems. With monetary policy in the G-33 remaining highly accommodative for the foreseeable future, the pace and quality of growth in EM—for example, the amount and type of issuance throughout the EM corporate credit space and the level of asset quality and leverage in EM banking systems—bears close monitoring to identify potential balance-sheet vulnerabilities percolating under the surface.

Bars represent the change in Total Sovereign Vulnerability Score between 2011 and 2008. The actual country score is based

on a

scale of 0 (low stress) to 10 (high stress) which reflects economic/financial risk based on select domestic/external indicators.

Q: Is EM debt still attractive versus EM equities?

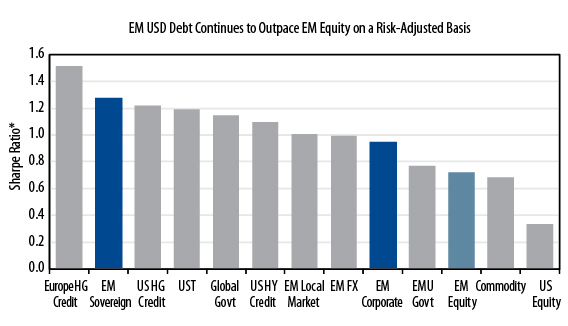

A: We believe so. Since the 2008 crisis, EM equity continues to outpace EM debt in terms of volatility. This year has been no different, with sharp bouts of market volatility stemming from US-, Europe- and China-related growth fears, helping to extend EM equities’ track record of poor risk-adjusted returns relative to EM debt. As a result, we’re seeing more traditional holders of EM equity considering a partial or outright reallocation to EM sovereign and/or corporate credit. This shift ininvestor mindset reflects a growing recognition that balance-sheet strength and policy flexibility in EM will likely be more supportive of EM debt valuations than EM equities, which remain more vulnerable to technical-driven rallies and further downward revisions to global growth. With intra-EM flows highlighting investors’ stronger preference for EM debt over EM equities, it’s difficult to see anything fundamental, barring a sudden and credible resolution of today’s major headline risks, that would change that dynamic anytime soon.

Q. Have you observed any new trends developing in the EM debt space?

A: We continue to see a meaningful bifurcation between the investment-grade-rated and high-yield-rated segments, which is the natural evolution of any growing bond market. Indeed, while investor demand remains strong for diversified and sector specific EM debt products (such as local markets or corporate credit), we’ve also seen growing

*Sharpe Ratios: Average annual returns since Jan 2003/Annualized standard deviation of monthly returns since Jan 2003.

Standard

deviation measures the volatility of an investment’s return over a particular time period; the greater the number, the

greater the volatility.

interest for customized and unconstrained (benchmark unaware) mandates that focus either on the higher liquidity and relative safety of investment-grade-rated sovereign and corporate debt, or the higher income and total return potential offered by highyield-rated EM assets. The latter trend has been a particularly interesting space to watch with the proliferation of new EM high-yield (EM HY) benchmarks and the launch of new (passively managed) Exchange Trade Funds (ETFs)4 in this sector. EM HY is an area that’s expected to grow further in the years ahead and one for which Western Asset is well positioned.

Q. How should investors be positioned in EM as we move into year-end?

A: Investors should brace for more headline-driven volatility throughout 4Q12. We have China “hard-landing” fears to consider, a leadership transition there in October, which could produce some policy surprises, the prospect of more political brinkmanship in the US following the presidential elections in November, which might result in another US ratings downgrade, the possibility of the European Central Bank once again having to defuse peripheral European tail risk, and the risk that more Middle East related turmoil will precipitate another sharp move in oil prices. Historically, the impact of one of these headlines has resulted in a higher degree of cross asset class correlation5 and sawtooth-shaped trading patterns.

If you consider the source of market volatility in EM over the past two years, most of it came from US dollar/euro volatility rather than an EM sovereign credit event or sharp, unexpected moves in EM local rates or US long-term interest rates. However, should global macro conditions stabilize or quantitative easing/growth-induced inflationary fears materialize, it would certainly heighten concerns over duration risk.

Weighing all of these fundamental factors along with the technical dynamics discussed earlier, it makes sense to focus on USD-denominated EM sovereign and corporate debt for their more defensive qualities—investors have more options to calibrate their liquidity, credit quality and duration preferences—and playing EM local markets only tactically. Investing in EM local markets certainly remains an attractive fundamental story over the long term, but in the near term, given the prevailing high and positive correlation of EM currencies to global markets and the possibility of another round of macroprudential measures (as EM policymakers attempt to mitigate the negative effects of open-ended quantitative easing by DM central banks), the risk/reward balance currently favors EM USD-denominated debt.

Q. Why should investors look to Western Asset for EM?

A: Western Asset has been involved in EM mandates since 1993 and dedicated EM strategies since 1996. As the EM universe has grown over the past 20 years, so has the depth of our collective experiences and our respect for what it takes to opportunistically navigate markets through smooth and turbulent times.

Western Asset’s EM effort is essentially an EM “boutique” supported by a global fixed-income powerhouse. Combined with our team culture and globally integrated investment approach, this arrangement has really contributed to our success in EM. With thirty dedicated EM professionals located in four offices on four continents, there’s a high degree of communication and collaboration and a passion for the countries and sectors they cover. In a new world order where the lines between the developed and emerging world continue to blur, having a top-down and bottom-up approach to global investing is essential; this is why the EM team has benefited greatly from the input it receives from seasoned professionals across various sector teams and from forums such as our Global Investment Strategy Committee and Global Credit Committee.

Our EM product line-up, which continues to evolve with the asset class, offers investors the ability to invest across the spectrum of EM debt. In a nervous market where risk sentiment can swing sharply from week to week, and there’s little consensus over what direction markets are headed toward over the medium term, we have the ability to rotate across all three sectors of the EM asset class—EM USD sovereigns, EM USD corporate credit, and EM local markets—seeking the opportunity to capture the best risk-adjusted returns possible. Alternatively, an investor can choose to focus on a specific sector, such as our EM corporate credit product, for which we have the longest track record in our peer group.

Given the events we’re seeing today, there’s no doubt that a paradigm shift is well underway in the global economy. These shifts, unfortunately, are never smooth and the trajectory of progress is rarely linear. The staying power of EM will depend in large part on how the developed world addresses its structural problems and whether EM can avoid policy mistakes that could potentially reverse years of hard-earned progress.

With this view of risk and reward, we believe a global story is best managed by a global firm in terms of scale and scope, and by a process such as Western Asset’s.

1. Gross Domestic Product (“GDP”) is an economic statistic which measures the market value of all final goods and services produced within a country in a given period of time.

2. “Net issuance of USD spread product peaked in 2006 at US$1.6 trillion and since has declined sharply, reaching US$462 billion in 2009 and expected to be US$264 billion in 2012.” JP Morgan, “EM Rerates as an Asset Class”, August 10, 2012

3. G-3 refers to the US, Europe and Japan.

4. An ETF is an unmanaged compilation of multiple individual securities and typically represents a particular securities index or sector of the securities market. Investors should carefully consider an ETF’s investment objectives, risks, charges and expenses before investing in an ETF.

5. Correlation is a statistical measure of the relationship between two sets of data. When asset prices move together, they are described as positively correlated; when they move opposite to each other, the correlation is described as negative. If price movements have no relationship to each other, they are described as uncorrelated.

Past performance is no guarantee of future results. Please note that an investor cannot directly invest in an index. This material is intended to provide Western Asset’s overall view and is not on behalf of any specific product or portfolio. All investments involve risk, including loss of principal. Fixed income securities are subject to interest rate and credit risk, which is a possibility that the issuer of a security will be unable to make interest payments and repay the principal on its debt. As interest rates rise, the price of fixed income securities falls. High yield bonds are subject to increased risk of default and greater volatility due to the lower credit quality of the issues. Foreign securities are subject to the additional risks of fluctuations in foreign exchange rates, changes in political and economic conditions, foreign taxation, and differences in auditing and financial standards. These risks are magnified in the case of investment in emerging markets.

U.S. Treasuries are direct debt obligations issued and backed by the “full faith and credit” of the U.S. government. The U.S. government guarantees the principal and interest payments on U.S. Treasuries when the securities are held to maturity. Unlike U.S. Treasury securities, debt securities issued by the federal agencies and instrumentalities and related investments may or may not be backed by the full faith and credit of the U.S. government. Even when the U.S. government guarantees principal and interest payments on securities, this guarantee does not apply to losses resulting from declines in the market value of these securities.

A credit rating is a measure of an issuer’s ability to repay interest and principal in a timely manner. The credit ratings provided by Standard and Poor’s, Moody’s Investors Service and/or Fitch Ratings, Ltd. typically range from AAA (highest) to D (lowest). Please see ww.standardandpoors.com, www.moodys.com, or www.fitchratings.com for details.

Yields represent past performance and there is no guarantee they will continue to be paid.

Diversification does not assure a profit or protect against market loss.

© Western Asset Management Company 2012. This publication is the property of Western Asset Management Company and is intended for the sole use of its clients, consultants and other intended recipients. It should not be forwarded to any other person. Contents herein should be treated as confidential and proprietary information. This information may not be reproduced or used in any form or medium without express written permission.

IN THE U.S. – INVESTMENT PRODUCTS: NOT FDIC INSURED • NO BANK GUARANTEE • MAY LOSE VALUE

Batterymarch • Brandywine Global • ClearBridge Advisors • Legg Mason Capital Management • Legg Mason Global Asset Allocation • Legg Mason Global Equities Group • Permal • Royce & Associates • Western Asset Management

This document is for information only and does not constitute an invitation to the public to invest. You should be aware that the investment opportunities described should normally be regarded as longer term investments and they may not be suitable for everyone. The value of investments and the income from them can go down as well as up and investors may not get back the amounts originally invested, and can be affected by changes in interest rates, in exchange rates, general market conditions, political, social and economic developments and other variable factors. Past performance is no guide to future returns and may not be repeated. Investment involves risks including but not limited to, possible delays in payments and loss of income or capital. Neither Legg Mason nor any of its affiliates guarantees any rate of return or the return of capital invested. Please note that an investor cannot invest directly in an index. Forward-looking statements are subject to uncertainties that could cause actual developments and results to differ materially from the expectations expressed. This information has been prepared from sources believed reliable but the accuracy and completeness of the information cannot be guaranteed and is not a complete summary or statement of all available data. Individual securities mentioned are intended as examples of portfolio holdings and are not intended as buy or sell recommendations. Information and opinions expressed by either Legg Mason or its affiliates are current as of the date indicated, are subject to change without notice, and do not take into account the particular investment objectives, financial situation or needs of individual investors. The information in this document is confidential and proprietary and may not be used other than by the intended user. Neither Legg Mason nor any officer or employee of Legg Mason accepts any liability whatsoever for any loss arising from any use of this document or its contents. This document may not be reproduced, distributed or published without prior written permission from Legg Mason. Distribution of this document may be restricted in certain jurisdictions. Any persons coming into possession of this document should seek advice for details of, and observe such restrictions (if any).

This document may have been prepared by an advisor or entity affiliated with an entity mentioned below through common control and ownership by Legg Mason, Inc.

This material is only for distribution in the jurisdictions listed.

Investors in Europe:

Issued and approved by Legg Mason Investments (Europe) Limited, registered office 201 Bishopsgate, London EC2M 3AB. Registered in England and Wales, Company No. 1732037. Authorized and regulated by the Financial Services Authority. Client Services +44 (0)207 070 7444. This document is for use by Professional Clients and Eligible Counterparties in EU and EEA countries. In Switzerland this document is only for use by Qualified Investors. It is not aimed at, or for use by, Retail Clients in any European jurisdictions.

Investors in Hong Kong, Korea, Taiwan and Singapore:

T his document is provided by Legg Mason Asset Management Hong Kong Limited in Hong Kong and Korea, Legg Mason Asset Management Singapore Pte. Limited (Registration Number (UEN ): 200007942R) in Singapore and Legg Mason Investments (Taiwan) Limited (Registration Number: (98) Jin Guan Tou Gu Xin Zi Di 001; Address: Suite E, 55F, Taipei 101 Tower, 7, Xin Yi Road, Section 5, Taipei 110, Taiwan, R.O.C.; Tel: (886) 2-8722 1666) in Taiwan. Legg Mason Investments (Taiwan) Limited operates and manages its business independently. It is intended for distributors use only in respectively Hong Kong, Korea, Singapore and Taiwan. It is not intended for, nor should it be distributed to, any member of the public in Hong Kong, Korea, Singapore and Taiwan.

Investors in the Americas:

This document is provided by Legg Mason Investor Services LLC, a U.S. registered Broker-Dealer, which may include Legg Mason International – Americas Offshore. Legg Mason Investor Services, LLC, Member FINRA/SIPC, and all entities mentioned are subsidiaries of Legg Mason, Inc.

Investors in Canada:

This document is provided by Legg Mason Canada Inc. Address: 220 Bay Street, 4th Floor, Toronto, ON M5J 2W4. Legg Mason Canada Inc. is affiliated with the Legg Mason companies mentioned above through common control and ownership by Legg Mason, Inc.

Investors in Australia:

T his document is issued by Legg Mason Asset Management Australia Limited (ABN 76 004 835 839, AFSL 204827) (“Legg Mason”). The contents are proprietary and confidential and intended solely for the use of Legg Mason and the clients or prospective clients to whom it has been delivered. It is not to be reproduced or distributed to any other person except to the client’s professional advisers.

This material is not for public distribution outside the United States of America.

Legg Mason Perspectives® is a registered trademark of Legg Mason Investor Services, LLC.