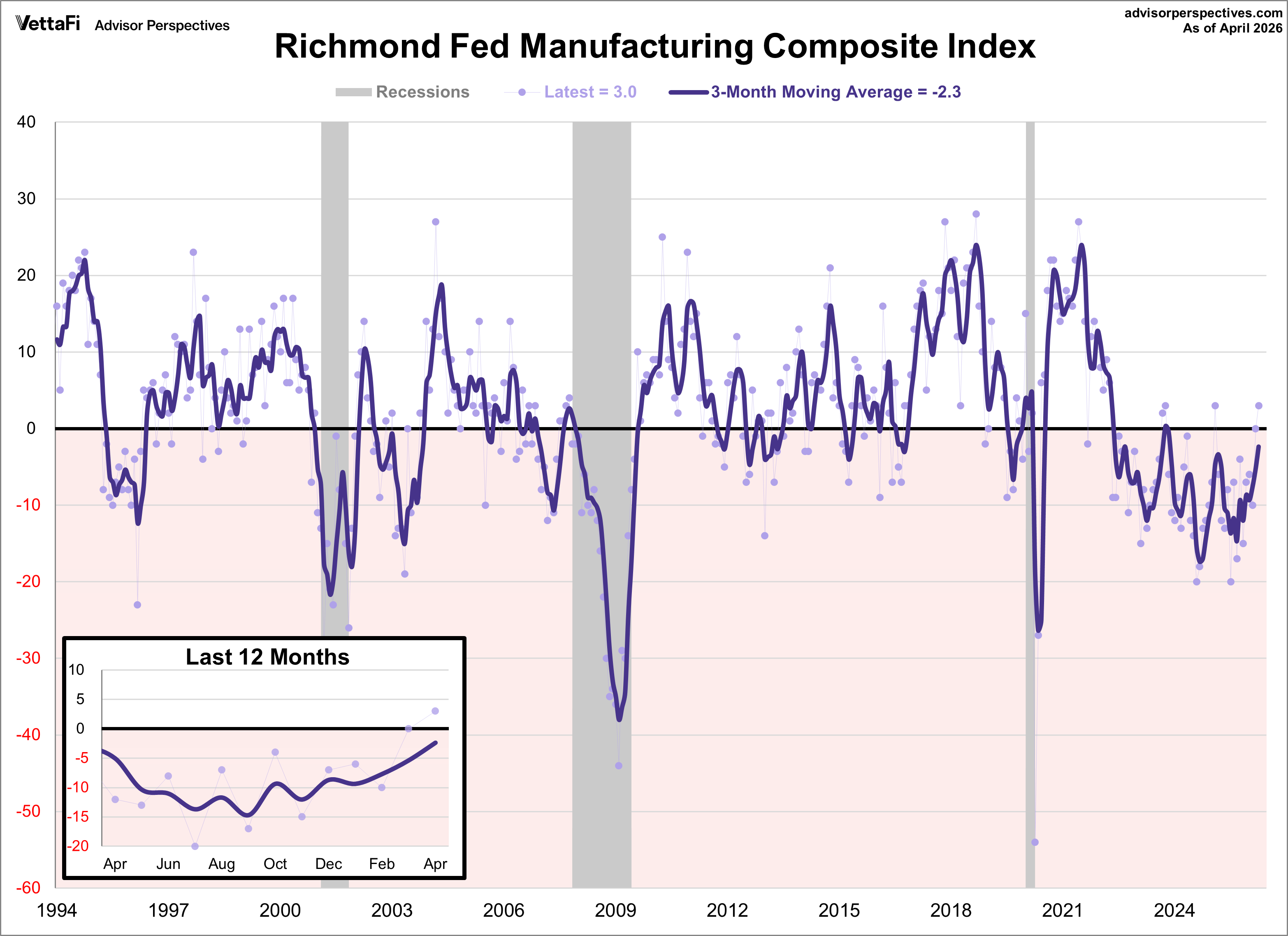

Fifth district manufacturing activity increased in April according to the most recent survey from the Federal Reserve Bank of Richmond. The composite manufacturing index rose three points points to 3, marking the highest level for the index in 20 months. This month's reading was above the forecast of 2.

Here is an excerpt from the latest Richmond Fed manufacturing report:

Fifth District manufacturing activity changed little in April, according to the most recent survey from the Federal Reserve Bank of Richmond. The composite manufacturing index inched up to 3 in April from 0 in March. Two of its three component indexes rose in April: new orders to 8 from 4 and employment to 0 from −2. Meanwhile, the shipments index was unchanged at −2 in April.

The local business conditions index increased to 10 in April from −5 in March. Meanwhile, the future local business conditions index decreased to 3 from 16. The future indexes for shipments and new orders also decreased slightly but remained solidly in positive territory. The expectations index for employment fell to 7 from 14.

The average growth rate of prices paid increased somewhat, while average growth in prices received decreased slightly in April. Firms expected growth in both price measures to moderate over the next 12 months.

Background on Richmond Fed Manufacturing

The complete data series behind today's Richmond Fed manufacturing report, which dates from November 1993, is available here. The Richmond Manufacturing Index is a gauge of manufacturing activity in the Fifth Federal Reserve District (Maryland, North Carolina, the District of Columbia, Virginia, most of West Virginia, and South Carolina) compiled from a survey of ~100 manufacturers. The composite manufacturing index is an average of indexes on shipments, new orders, order backlogs, capacity utilization, supplier lead times, number of employees, average work weak, wages, inventories, and capital expenditures. This is a diffusion index, meaning negative readings indicate contraction and worsening conditions, while positive ones indicate expansion and improving conditions. The survey offers clues on inflationary pressures and the pace of growth in the manufacturing sector for this region of the country and the accumulated results can help trace long-term trends.